Informal savings groups, which are often referred to as Rotating Savings and Credit Associations (ROSCAs), Accumulating Savings and Credit Associations (ASCAs), Village Savings and Loan Associations (VSLAs), Village Community Banks (VICOBA) or Community Microfinance Groups (CMGs), hold a significant importance in African communities. They reflect a long-standing tradition of resilience and financial practices, particularly among women in low-income households and rural areas. These groups typically operate outside the formal financial system, leading to a limited acknowledgement of their members’ credit histories by financial institutions. However, there is potential for this dynamic to evolve.

In Tanzania, CMGs are vital in promoting financial inclusion, accounting for 12% of the nation’s overall adult population.1 These groups provide a crucial platform for savings, enabling roughly 5 million adults to participate actively in building their financial stability. Through their collective efforts, members of the groups are empowered to save, invest, and improve their economic well-being, contributing significantly to the country’s development.

The question of whether to digitize the operations or transactions of informal savings groups has generated varied opinions. Some argue that digitization could introduce several challenges, such as the potential loss of informal benefits like social cohesion and flexibility, privacy and security concerns, the costs associated with digitization, digital illiteracy, and the impact of social norms. On the other hand, proponents believe digitization is key to enhancing financial inclusion—especially for women—improving convenience in cash handling, enabling access to value-added services, and promoting transparency and accountability. Despite the skepticism surrounding this transition, it is evident that digitization represents an effort to bridge the gap between formal and informal financial systems.2

In 2023, a significant step was taken to enhance financial inclusion in Tanzania through a collaboration between the Financial Sector Deepening Tanzania (FSDT), Mixx by Yas, formerly known as TigoPesa-a Mobile Network Operator (MNO)-and the Financial Sector Deepening (FSD) Network Gender Collaborative Programme. As a key facilitator of financial Market Systems Development (MSD), FSDT, in partnership with the FSD Network Gender Collaborative Programme, is at the forefront of initiatives that harness the full potential of Digital Financial Services (DFS). Prior to the implementation of the project, the partners’ mission was to create and unlock significant DFS opportunities for women in Tanzania, hence the bold attempt to support Mixx by Yas in digitizing CMGs’ transactions.

In 2023, a significant step was taken to enhance financial inclusion in Tanzania through a collaboration between the Financial Sector Deepening Tanzania (FSDT), Mixx by Yas, formerly known as TigoPesa-a Mobile Network Operator (MNO)-and the Financial Sector Deepening (FSD) Network Gender Collaborative Programme. As a key facilitator of financial Market Systems Development (MSD), FSDT, in partnership with the FSD Network Gender Collaborative Programme, is at the forefront of initiatives that harness the full potential of Digital Financial Services (DFS). Prior to the implementation of the project, the partners’ mission was to create and unlock significant DFS opportunities for women in Tanzania, hence the bold attempt to support Mixx by Yas in digitizing CMGs’ transactions.

The partnership aimed to promote the digitization of transactions within CMGs, while advancing a strategic vision of expanding financial service accessibility and interoperability, enabling members to participate regardless of their MNOs. The foundation for this effort stems from the Tanzanian Government’s initiative that formally recognizes these groups as tier 4 under the Microfinance Act of 2018. This legislation enabled the Bank of Tanzania (BOT) through President’s office Regional Administration and Local Government (PO-RALG) to create an online registration system, resulting in the successful registration of over 48,659 CMGs throughout the country. This development presents an extraordinary opportunity for innovation in what was generally operating informally.

The urgency for this initiative was underscored by the lessons gathered from previous groups digitization initiative by FSDT in collaboration with Vodacom Mpesa (MKOBA product) and Tanzania Commercial Bank (TCB), the bank behind digitization of groups’ transactions in

partnership with MNOs as well as insights from the FinScope Tanzania 2023 report, which revealed compelling trends among rural populations. Many individuals in rural areas tend to save their money at home, often relying on informal savings mechanisms. Notably, women exhibit a stronger preference for these methods—53% of the adult population engages in home savings, and their participation in CMGs is impressively 7% higher than that of men. This data highlights the crucial role women play in community financial practices and underscores the potential impact of introducing digital financial solutions tailored to their needs.

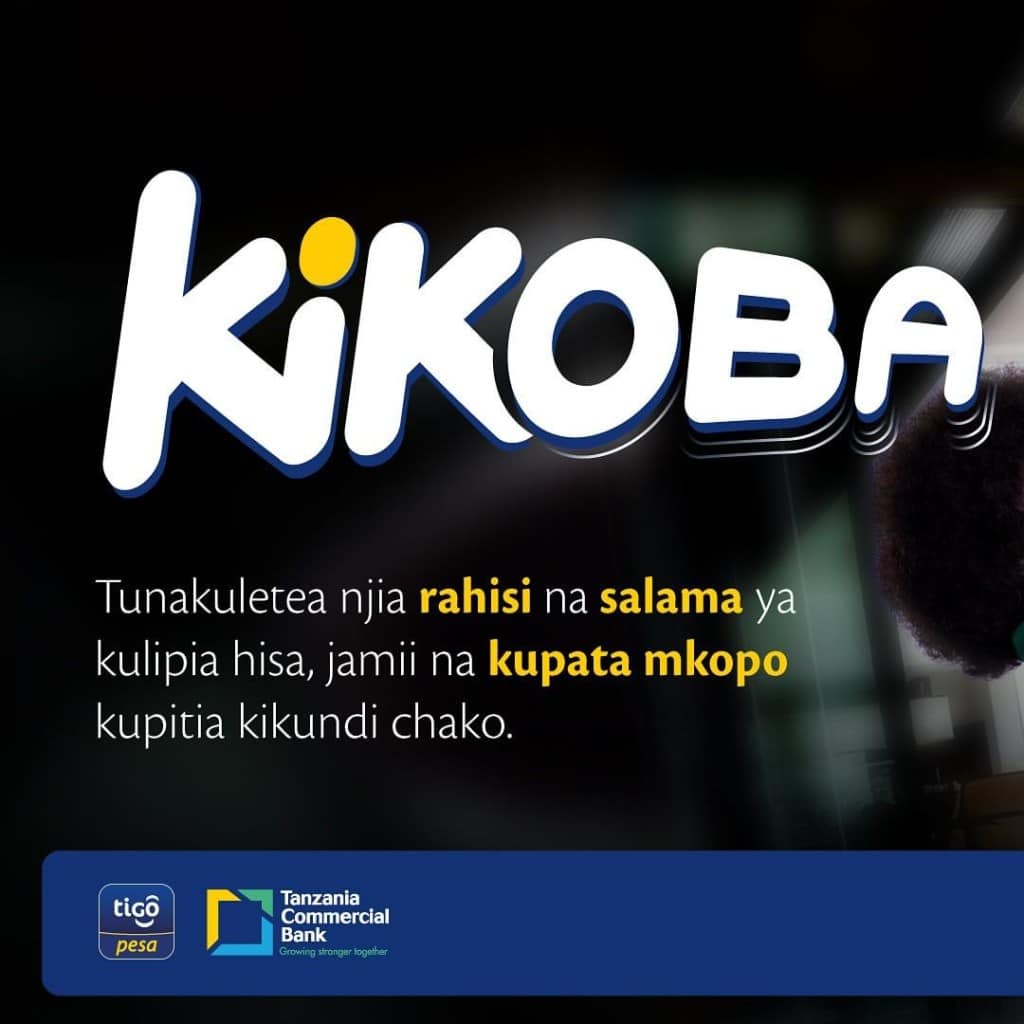

In April 2024, Mixx by Yas through its partnership with TCB and the support from FSDT, launched ‘Tigo Kikoba’ currently known as Mixx Kikoba—a digital product that streamlines all financial operations for group members. Through this platform, all members can access the group’s savings and loan activities. Instead of keeping cash in a physical box as traditionally done, the money is now stored in a digital account, and transaction records have been automated. The launch was accompanied by a series of customized training activities for the community development offers (CDOs), community-based trainers (CBTs) and promoters of the savings groups, who in turn trained the members of the savings groups – this was to ensure that group members were adequately resourced for the use of the ‘Mixx Kikoba’. As a pilot, three regions were selected based on two main factors, which are the region that is least financially included and the regions where Yas had the highest market share. Such regions were Singida, Morogoro, and Tabora, in which over 600 CBTs and CDOs were trained. The bundled capacity-building component and awareness creation went a long way to familiarise the members with the product, leading to onboarding over 15,000 CMGs as early adopters nationwide. In addition, Yas implemented a comprehensive communication strategy to enhance awareness of the product, ensuring that the messaging was done in Kiswahili, which is the dominant language of the Tanzanian consumer as attested by the FinScope Tanzania 2023 survey (79% of Tanzanians can read and write in Kiswahili). This communication strategy utilized informative brochures and radio broadcasts to effectively disseminate information. By employing these methods, Mixx by Yas successfully communicated the product’s value and benefits to a broad audience.

In April 2024, Mixx by Yas through its partnership with TCB and the support from FSDT, launched ‘Tigo Kikoba’ currently known as Mixx Kikoba—a digital product that streamlines all financial operations for group members. Through this platform, all members can access the group’s savings and loan activities. Instead of keeping cash in a physical box as traditionally done, the money is now stored in a digital account, and transaction records have been automated. The launch was accompanied by a series of customized training activities for the community development offers (CDOs), community-based trainers (CBTs) and promoters of the savings groups, who in turn trained the members of the savings groups – this was to ensure that group members were adequately resourced for the use of the ‘Mixx Kikoba’. As a pilot, three regions were selected based on two main factors, which are the region that is least financially included and the regions where Yas had the highest market share. Such regions were Singida, Morogoro, and Tabora, in which over 600 CBTs and CDOs were trained. The bundled capacity-building component and awareness creation went a long way to familiarise the members with the product, leading to onboarding over 15,000 CMGs as early adopters nationwide. In addition, Yas implemented a comprehensive communication strategy to enhance awareness of the product, ensuring that the messaging was done in Kiswahili, which is the dominant language of the Tanzanian consumer as attested by the FinScope Tanzania 2023 survey (79% of Tanzanians can read and write in Kiswahili). This communication strategy utilized informative brochures and radio broadcasts to effectively disseminate information. By employing these methods, Mixx by Yas successfully communicated the product’s value and benefits to a broad audience.

Conversations with some early adopters revealed that the savings groups, predominantly consisting of women, are already experiencing several benefits from using Mixx Kikoba leading to significantly transformed user experience. Such benefits include heightened cash security, giving them peace of mind as they manage their finances. The transition to digital wallets has not only safeguarded their funds but also served as a bulwark against past thefts that had once threatened their trust.

")